New Procedures for Preliminary Refund of Tax Overpayment

- May 26, 2026

- Posted by: Bella Rachmafanny

- Category: Tax Updates

Ref: Minister of Finance Regulation Number 28 of 2026 (PMK-28/2026)

The Ministry of Finance of the Republic of Indonesia officially issued Minister of Finance Regulation (PMK) Number 28 of 2026 on 29 April 2026, which came into effect on 1 May 2026 (PMK-28). This regulation revokes and replaces the previous regulatory framework, namely PMK-39/PMK.03/2018 as most recently amended by PMK No. 119 of 2025. This update is intended to ensure that the preliminary refund facility is granted in a more targeted manner, while maintaining a balance between the fulfillment of taxpayers’ rights and obligations. Upon the effective date of this Ministerial Regulation, Minister of Finance Regulation Number 39/PMK.03/2018 concerning the Procedures for Preliminary Refund of Tax Overpayment, along with its first, second, and third amendments, is hereby revoked and declared null and void.

In general, PMK-28/2026 does not eliminate taxpayers’ entitlement to preliminary refunds; rather, it introduces stricter provisions for taxpayers intending to apply for a preliminary refund of tax overpayments. The taxpayers eligible to apply for a preliminary refund are as follows:

– Taxpayers with Certain Criteria;

– Taxpayers Meeting Certain Requirements; and

– Low-Risk Taxable Entrepreneurs.

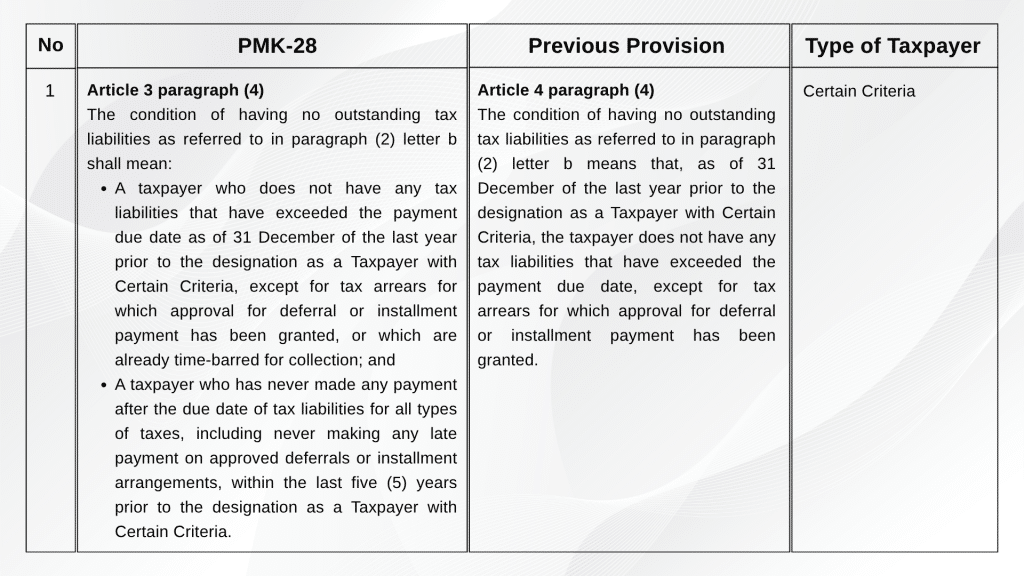

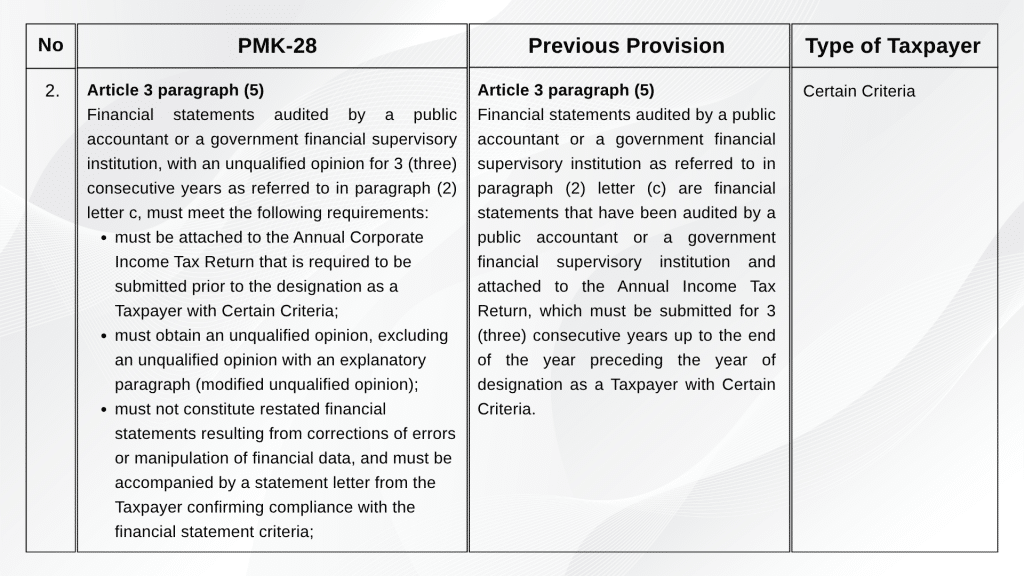

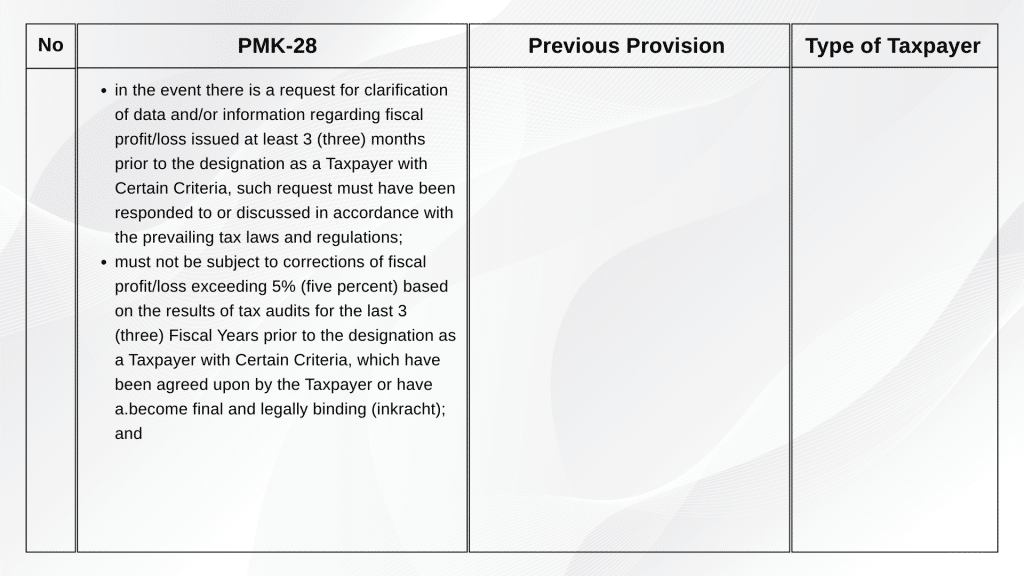

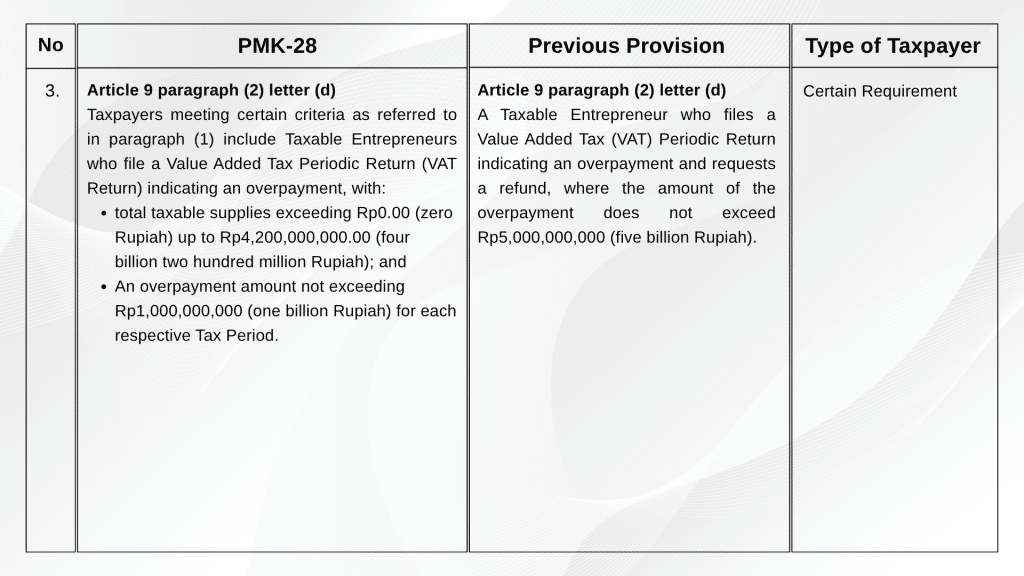

Under PMK-28, there is an expansion of provisions as well as a change in the limitations on applications for preliminary refunds compared to the previous regulation. The key changes are outlined below:

Furthermore, PMK-28 stipulates that taxpayers whose designation decisions are declared invalid, as referred to in letter (a), may reapply for designation as taxpayers with certain criteria from 1 June 2026 to 10 June 2026, or in accordance with the date referred to in Article 4 paragraph (1), i.e., 10 January. Such taxpayers may subsequently be designated as taxpayers with certain criteria within 30 (thirty) working days from the date of application submission, provided that they meet the requirements set out in Article 3 of PMK-28.

Through these regulatory changes introduced under PMK-28, it is expected that taxpayer compliance—particularly among those applying for preliminary tax refunds—will improve, while also providing greater legal certainty.

Effective Date: 1 May 2026