Indonesian Government Tightens the Tax Facility for SMEs and Strengthens Anti-Avoidance Rules

- June 15, 2026

- Posted by: Bella Rachmafanny

- Category: Tax Updates

The Government of Indonesia has issued Government Regulation (GR) No. 20 of 2026 (“PP-20”) as an amendment to GR No. 55 of 2022 (“PP-55”) on Adjustments to Income Tax Regulations. This amendment officially became effective on 22 April 2026.

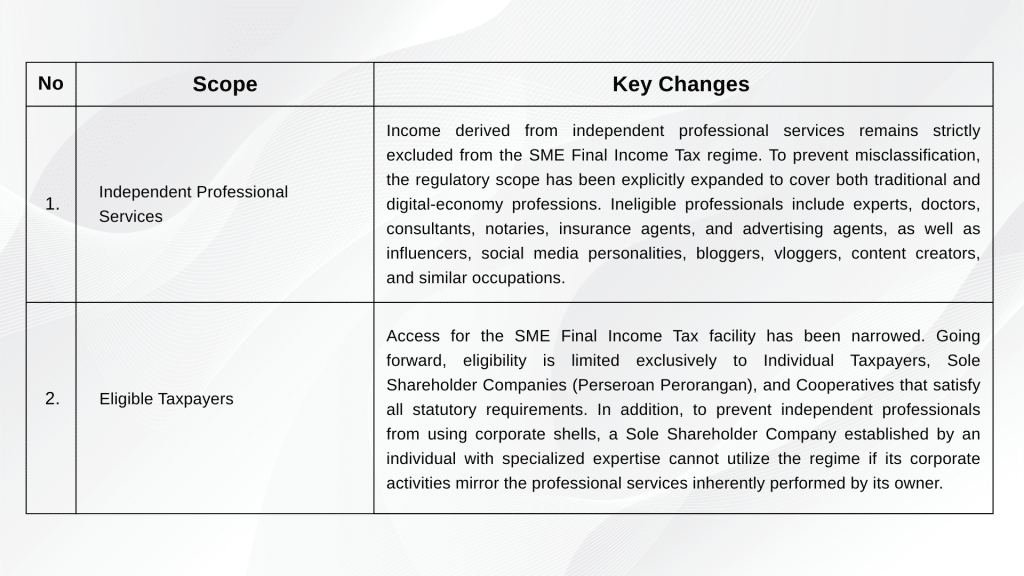

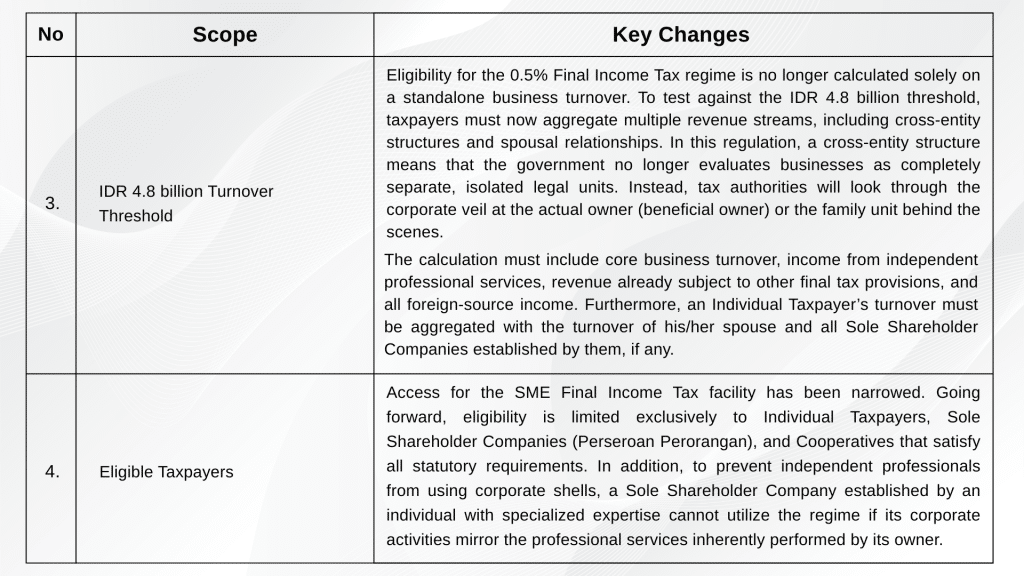

While PP-20 preserves the beneficial 0.5% Final Income Tax rate for Micro, Small, and Medium Enterprises (SMEs), it introduces new measures aimed at preventing tax avoidance practices, including business fragmentation and the use of legal entities for activities that are essentially independent professional services.

The scope and key changes include:

Under the transitional provisions of PP-20, corporate taxpayers that are already registered and utilizing the SME facility under PP-55 are not required to switch to the normal corporate tax rate immediately in the middle of the tax year. This transitional provision allows these companies to continue applying the 0.5% Final Income Tax rate for their remaining utilization period (such as the standard 3-year limit for corporate entities), provided they structurally met the initial requirements.

However, because the new rules change how the IDR 4.8 billion threshold is calculated (by aggregating all cross-entity and spousal revenues), their eligibility for the following tax year will depend on their new consolidated economic capacity. Therefore, existing corporate taxpayers utilizing this SME facility should thoroughly review whether the 0.5% Final Income Tax rate can still legally apply to them for the subsequent tax years under these new transitional dynamics.

In addition, to align with the OECD’s recommendation on combating international bribery and corruption, PP-20 introduces a critical amendment to the general income tax framework. The regulation explicitly states that expenses arising from bribes, gratuities, or any payments constituting corruption offenses (including those to foreign public officials) are strictly non-deductible for income tax purposes across all taxpayer categories.

Through these amendments, the Government continues to provide support for SMEs, while safeguarding the facility to be utilized only by eligible taxpayers. The new PP-20 also promotes a fairer tax system, enhances legal certainty, and minimizes opportunities for tax avoidance.