INTERNAL MEMO NUMBER ND-1/PJ/PJ.02/2026

- March 16, 2026

- Posted by: Bella Rachmafanny

- Category: Tax News

The Directorate General of Taxes (DGT) has issued Internal Memo Number ND-1/PJ/PJ.02/2026 to clarify the taxation of domestic dividends. This move tightens supervision over dividends distributed without a formal General Meeting of Shareholders (GMS/RUPS).

For businesses, this is a critical reminder that procedural compliance is mandatory to enjoy the dividend tax exemption facility.

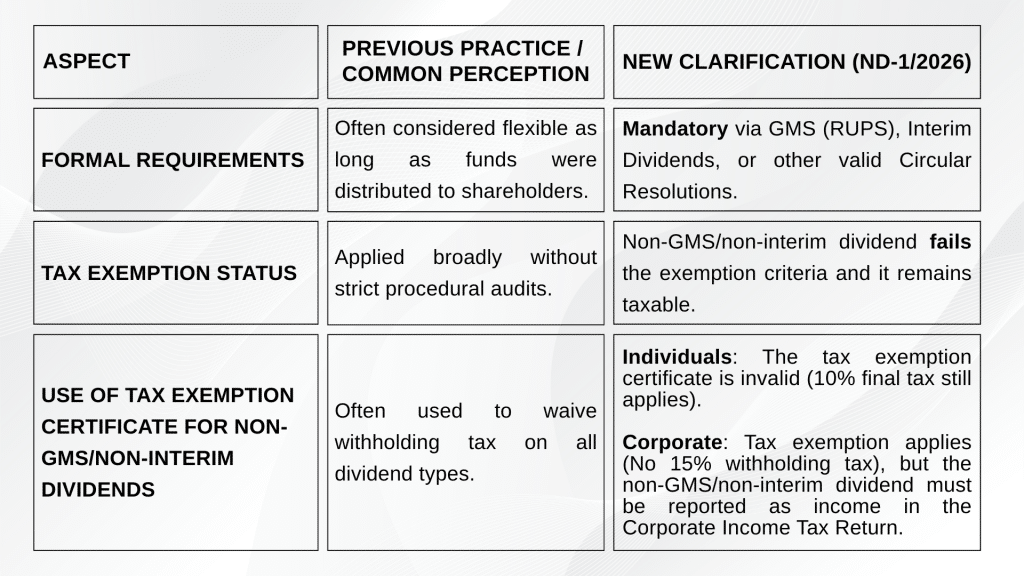

Policy Transformation: What Has Changed?

Previously, many businesses assumed all dividend distributions were automatically tax-exempt. The following table highlights the crucial changes:

Procedural Formality: The Key to Tax Exemption

ND-1/2026 emphasizes that tax exemption only applies if the distribution follows corporate legal standards, including:

- A valid General Meeting of Shareholders (RUPS).

- Interim Dividends in accordance with the Company’s Articles of Association.

- Circular Resolutions signed by all shareholders with voting rights.

Tax Consequences and “Hidden Dividends”

If the distribution occurs outside these formal channels, the payer must withhold tax as follows:

- Domestic Individual Taxpayers: Subject to a 10% Final Tax.

- Domestic Corporate Taxpayers/Permanent Establishments: Subject to 15% Withholding Tax (Article 23).

- Foreign Taxpayers: Subject to 20% Withholding Tax (Article 26) or applicable Tax Treaty rates.

The DGT also warns against “Hidden Dividends” (e.g., company expenses for personal shareholder interests or excessive loan interest), which will be reclassified and taxed as dividends.

Effective Date

Issued on February 3, 2026, this Note is marked as “Immediate” and serves as a direct guideline for tax offices to monitor compliance in the field.